All Categories

Featured

Table of Contents

I paid into Social Safety for 26 years of considerable incomes when I was in the private field. I do not want to return to work to obtain to 30 years of substantial incomes in order to prevent the windfall elimination provision reduction.

I am paying every one of my bills currently yet will do even more traveling when I am gathering Social Protection. Should I wait up until 70 to collect? I assume I need to live till regarding 84 to make waiting a great selection. I attempted to get this response from an economic planner at a free workshop and he would certainly not inform me without hiring him for additional assessments.

If your Social Safety benefit is truly "fun cash," as opposed to the lifeline it functions as for lots of people, maximizing your advantage may not be your top priority. However obtain all the info you can about the price and advantages of asserting at different ages before making your choice. Liz Weston, Licensed Financial Organizer, is a personal finance columnist for Concerns might be sent to her at 3940 Laurel Canyon Blvd., No.

Cash money value can collect and expand tax-deferred inside of your policy. It's essential to keep in mind that impressive policy lendings build up rate of interest and decrease cash worth and the fatality advantage.

Nevertheless, if your cash worth falls short to grow, you may require to pay greater costs to keep the plan effective. Plans may use different alternatives for growing your money value, so the crediting rate relies on what you choose and just how those options do. A set sector earns rate of interest at a defined rate, which might change in time with financial problems.

Neither kind of policy is necessarily much better than the other - all of it boils down to your goals and approach. Entire life plans may appeal to you if you like predictability. You know specifically just how much you'll need to pay each year, and you can see how much money value to expect in any kind of provided year.

North American Universal Life Insurance

When assessing life insurance policy needs, review your long-term goals, your current and future expenditures, and your desire for safety. Review your objectives with your agent, and select the policy that functions best for you. * As long as needed premium payments are prompt made. Indexed Universal Life is not a safety financial investment and is not an investment in the marketplace.

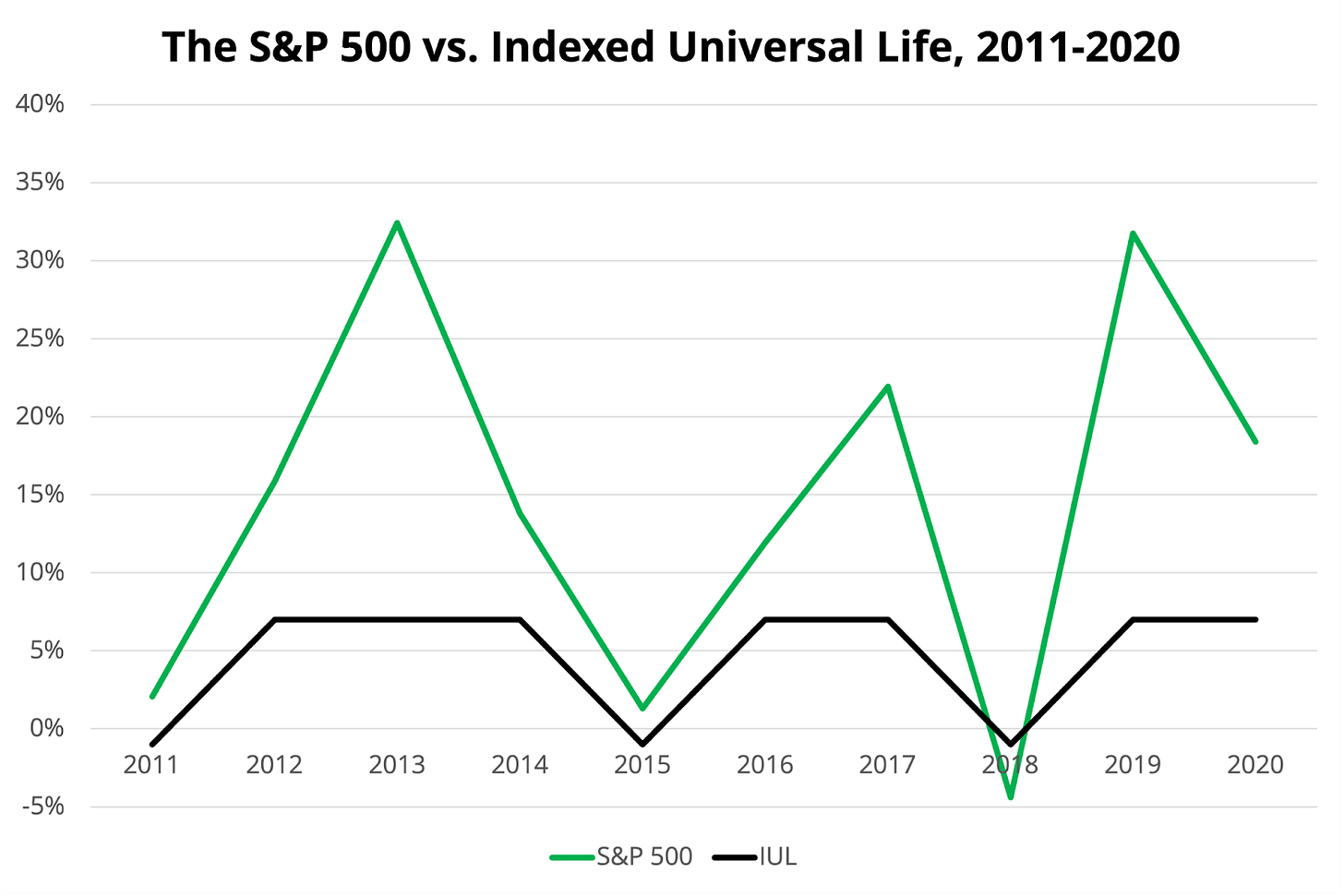

Last year the S&P 500 was up 16%, but the IULs development is capped at 12%. That doesn't seem regrettable. 0% flooring, 12% potential! Why not?! Well, a couple things. These IULs overlook the existence of rewards. They take a look at just the adjustment in share rate of the S&P 500.

What Is The Difference Between Term And Universal Life Insurance

Second, this 0%/ 12% game is primarily a shop technique to make it seem like you always win, however you don't. In the last 40 years, the S&P 500 was up 31 years. 21 of those were above 12%, balancing virtually 22%. It ends up losing out on the substantial development hurts you way greater than the 0% disadvantage helps.

:max_bytes(150000):strip_icc()/pros-cons-indexed-universal-life-insurance.asp_v1-e119226901bc464593a496c003551ea0.png)

If you need life insurance policy, acquire term, and invest the remainder. -Jeremy by means of Instagram.

Your existing browser could limit that experience. You may be utilizing an old browser that's in need of support, or setups within your internet browser that are not suitable with our site.

Your current web browser: Spotting ...

You will have to provide certain supply about yourself and your lifestyle in way of life to receive an indexed universal life global quoteInsurance policy Cigarette smokers can anticipate to pay greater premiums for life insurance policy than non-smokers.

Indexed Universal Life Insurance Pros And Cons

If the policy you're looking at is traditionally underwritten, you'll require to finish a clinical exam. This test involves conference with a paraprofessional who will certainly get a blood and urine sample from you. Both samples will certainly be examined for possible health and wellness threats that can influence the kind of insurance policy you can get.

Some variables to take into consideration include the number of dependents you have, the amount of earnings are coming into your home and if you have costs like a mortgage that you would certainly desire life insurance policy to cover in the event of your fatality. Indexed universal life insurance policy is just one of the more complex types of life insurance policy presently readily available.

If you're trying to find an easy-to-understand life insurance coverage plan, nonetheless, this may not be your best alternative. Prudential Insurance Coverage Company and Voya Financial are some of the greatest carriers of indexed universal life insurance policy. Voya is thought about a top-tier provider, according to LIMRA's 2nd quarter 2014 Final Costs Coverage. While Prudential is a historical, very respected insurance coverage firm, having actually been in service for 140 years.

Pros And Cons Of Indexed Universal Life Insurance

On April 2, 2020, "A Vital Review of Indexed Universal Life" was made available through various outlets, including Joe Belth's blog site. Not surprisingly, that piece created substantial remarks and objection.

Some disregarded my remarks as being "persuaded" from my time helping Northwestern Mutual as an office actuary from 1995 to 2005 "normal whole lifer" and "prejudiced versus" products such as IUL. There is no challenging that I helped Northwestern Mutual. I enjoyed my time there; I hold the business, its staff members, its products, and its mutual philosophy in high respect; and I'm happy for every one of the lessons I found out while employed there.

I am a fee-only insurance consultant, and I have a fiduciary obligation to watch out for the finest interests of my customers. By interpretation, I do not have a predisposition toward any type of product, and in reality if I discover that IUL makes sense for a customer, after that I have a responsibility to not just existing however advise that choice.

I constantly strive to place the best foot ahead for my customers, which implies utilizing styles that decrease or remove payment to the best degree feasible within that certain policy/product. That does not constantly suggest recommending the plan with the lowest settlement as insurance is much more complex than just contrasting payment (and occasionally with items like term or Assured Universal Life there merely is no compensation adaptability).

Some recommended that my level of interest was clouding my reasoning. I like the life insurance policy industry or a minimum of what it can and need to be (best indexed universal life insurance). And indeed, I have an amazing quantity of interest when it involves really hoping that the sector does not get yet another shiner with extremely hopeful pictures that set customers up for disappointment or worse

Iul Pros And Cons

I might not be able to transform or conserve the sector from itself with respect to IUL products, and truthfully that's not my objective. I want to aid my customers take full advantage of value and prevent important mistakes and there are customers out there every day making poor decisions with regard to life insurance policy and particularly IUL.

Some people misconstrued my criticism of IUL as a blanket recommendation of all things non-IUL. This might not be better from the reality. I would not personally suggest the huge majority of life insurance policy plans in the industry for my customers, and it is uncommon to find an existing UL or WL policy (or proposal) where the visibility of a fee-only insurance policy expert would certainly not include considerable customer value.

{kind=link}

Latest Posts

What Is Equity Indexed Universal Life Insurance

Best Universal Life Insurance

Guaranteed Death Benefit Universal Life